Q&A: Rolls-Royce CEO on the luxury business, the global economy, and building a $25M car

January 1, 2024

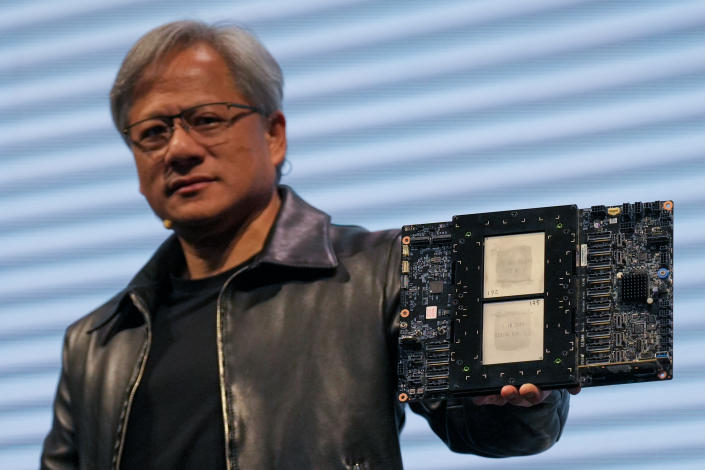

Nvidia stock soars to record high as earnings, forecasts crush expectations

January 1, 2024

How much money can I give to my son and daughter-in-law without incurring a tax issue with the IRS?

-Irwin

For 2023, you can give your son and daughter-in-law each $17,000 without having to deal with the IRS. But even if you give more, you won’t have to pay any taxes right now. In fact, unless you surpass the lifetime limit, currently around $12 million, you won’t have to pay any gift taxes.

An experienced financial advisor can help you navigate those rules, so you can continue to give gifts to the people you love without having to worry about gift taxes.

What Is Gift Tax?

The gift tax is a federal tax that may be imposed when you give someone property or money, and they don’t give you something of equal value in return. The IRS sets limits on how much you can give other people each year and over your lifetime. If you give more, you could end up owing taxes, but not until you cross the lifetime limit.

Gift tax rates are steep, starting at 18% and topping out at 40%. The person giving the gift pays the tax. (A financial advisor may be able to help you navigate the tax consequences of your gifting strategy.)

Gift Limits and Lifetime Exemptions

The annual gift limit usually changes every year. For 2023, the limit is $17,000. That means you can give anyone up to $17,000 without having to deal with the gift tax.

There’s no limit on how many people can receive your gift. So you could hand out $17,000 to 10 people and not trigger any annual gift tax issues. You can also give the same person up-to-the-limit gifts every year with no tax implications.

If any gift exceeds the annual limit, you’ll file a gift tax return on IRS Form 709. This is purely an informational return with no tax due until you cross the lifetime limit of $12,092,000 (for 2023). Only the excess portion of the gift starts to whittle down that lifetime exemption. For example, if you gave your niece $20,000 in 2023, you would file a gift tax return and deduct $3,000 of that from the lifetime exemption.

If you’re ready to be matched with local advisors that can help you achieve your financial goals, get started now.

What Counts as a Gift?

Any time you give someone money or property, and they don’t return something of equal (or close to equal) value, that counts as a gift. For example, if you give your sister your old car when you get a new one, that’s a gift. Other examples include contributing $20,000 to your grandchild’s 529 plan or treating your best friend to an all-expenses-paid vacation.

The IRS may also consider interest-free loans or loans that don’t get paid back as gifts. Another sticky situation: joint bank accounts with nonspouses. If you have a joint bank account with your adult child, a romantic partner or a sibling, large withdrawals could trigger the need to file a gift tax return.

Some types of gifts are tax-free and never count toward the lifetime limit. Those include:

Charitable donations

Political contributions

Gifts to spouses

Gifts to dependents

Medical expenses

Tuition payments

Medical expenses and tuition payments only count as nontaxable gifts if the payments are made directly to the school or healthcare provider on behalf of the giftee. (A financial advisor may be able to help you navigate the tax consequences of your gifting strategy.)

Special Gift Tax Strategies

If you’re likely to come up against that lifetime limit, there are moves you can make to reduce your chances of eventually owing gift taxes.

If you’re married, you can use a gift-splitting strategy. Here, you and your spouse can each give the annual limit to the same person with no tax fallout. For example, in 2023 you could each separately gift $17,000 to an adult child for a total $34,000 nontaxable gift, but if just one of you gave the full amount it would trigger Form 709.

There’s also a special rule that allows gift-givers to contribute $85,000 (in 2023) to a qualified tuition plan (QTP) and use up five years’ worth of exclusions so as not to exceed the annual gift limit. You’d have to file Form 709 in the first year to report that choice, but not in the following years unless you make additional gifts to the same recipient.

For future planning, you’ll want to make larger gifts before the lifetime limits revert to the much lower pre-2018 levels in 2026. Then, unless there are more rule changes, the lifetime limit will shrink back to about $5.5 million (adjusted for inflation). (A financial advisor may be able to help you navigate tax law changes and how they could impact you.)

Bottom Line

Most people won’t pay gift taxes. But you could end up needing to file a gift tax return in a year that you give generously to friends or family if you give more than the annual limit to any one person. For example, paying for a wedding, giving a car as a graduation gift or making a large interest-free loan that doesn’t get paid back could all potentially trigger Form 709.